Stocks Stage a Modest Retreat

The Week on Wall Street

Investors reacted to two major news items last week, one far more of a surprise than the other. The Federal Reserve did indeed make a rate cut, matching Wall Street expectations. Drone strikes on two of the world’s largest oil fields brought a shock to the global oil market.

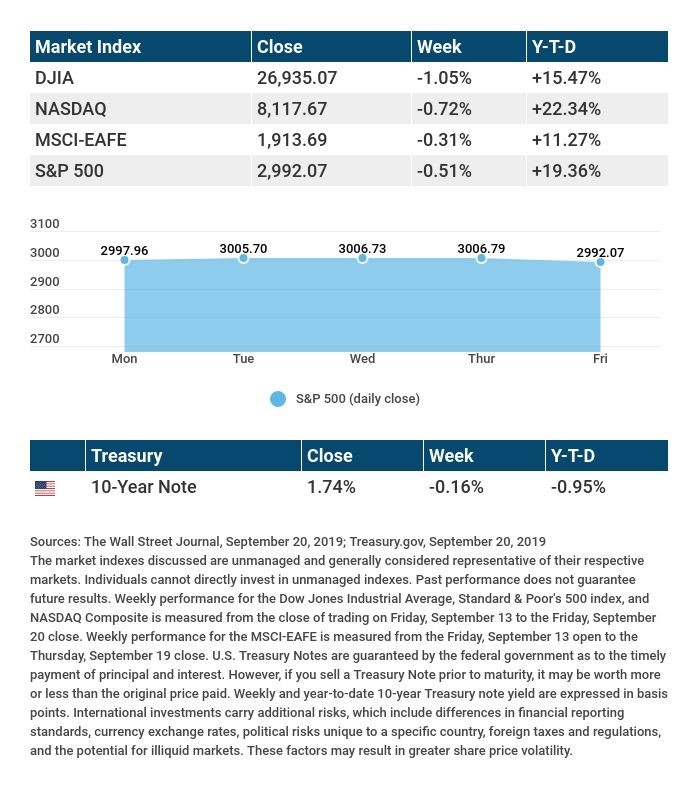

At Friday’s closing bell, stocks wound up with weekly losses after news broke that Chinese trade officials were heading home from the U.S. sooner than planned. The S&P 500 retreated 0.51% week-over-week; the Dow Jones Industrial Average lost 1.05%, and the Nasdaq Composite dipped 0.72%. In developed foreign markets, shares tracked by the MSCI EAFE index fell 0.31%.[i],[ii],[iii]

Another Quarter-Point Cut

Wednesday, the Federal Open Market Committee voted 7-3 to lower the benchmark interest rate by another 0.25%, to a range of 1.75% to 2.00%.

While traders looked for signs of future guidance on monetary policy, little emerged from the latest Fed policy statement and Fed chair Jerome Powell’s subsequent press conference. The updated dot-plot forecast showed that seven Fed officials anticipated at least one more cut before 2020, while ten did not.[iv]

Oil Prices Jump

As last week began, crude oil futures spiked in response to an attack that interrupted roughly 5% of the world’s oil production. The value of West Texas Intermediate crude, the U.S. benchmark, spiked 14.7% in a day, or $8.05 to $62.90 at Monday’s close.

This was oil’s biggest one-day leap since September 2008. Prices came down from there: Friday, WTI crude settled at $58.48.[v],[vi]

Final Thought

So, what day last week saw the biggest loss or gain for stocks? Not Monday, when the market absorbed news of the Saudi oil field strike. Not Wednesday, when the Fed rate cut occurred. Instead, it was Friday, when the S&P 500 lost only 0.49%. It just goes to show that stocks may ride through seemingly market-moving events with little daily change.[vii]

THE WEEK AHEAD: KEY ECONOMIC DATA

Tuesday: The Conference Board’s September Consumer Confidence Survey.

Wednesday: August new home sales data from the Census Bureau.

Thursday: The federal government’s third estimate of second-quarter economic growth.

Friday: August personal spending numbers from the Bureau of Economic Analysis, and September’s final University of Michigan Consumer Sentiment Index, measuring consumer confidence levels.

Source: Econoday, September 20, 2019

The Econoday economic calendar lists upcoming U.S. economic data releases (including key economic indicators), Federal Reserve policy meetings, and speaking engagements of Federal Reserve officials. The content is developed from sources believed to be providing accurate information. The forecasts or forward-looking statements are based on assumptions and may not materialize. The forecasts also are subject to revision.

THE WEEK AHEAD: COMPANIES REPORTING EARNINGS

Tuesday: AutoZone (AZO), Cintas (CTAS), Nike (NKE)

Thursday: Accenture (ACN), Carnival (CCL), Micron Technology (MU)

Source: Zacks, September 20, 2019

Companies mentioned are for informational purposes only. It should not be considered a solicitation for the purchase or sale of the securities. Any investment should be consistent with your objectives, time frame and risk tolerance. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. Companies may reschedule when they report earnings without notice.

[i] https://www.marketwatch.com/story/dow-skids-to-friday-lows-amid-reports-that-chinas-delegation-has-canceled-a-tariff-related-visit-2019-09-20

[iv] https://www.reuters.com/article/us-usa-fed/fed-cuts-rates-on-7-3-vote-gives-mixed-signals-on-next-move-idUSKBN1W32H7